Market Update & Economic Summary:

2015 market results were unremarkable. The DOW 30 returned -2.2%. The S&P 500 returned -0.7%. The broad markets fared less favorably with the average large stock dropping by 4%; roughly 37% of mid-cap stocks declined by 20% or more, while 46% of the small-cap stocks were down over 20%. The S&P suffered a 12% correction extending from early-August through mid-September in response to Chinese currency devaluation. The MSCI EAFE International Stock index dropped 3.3%. By year-end we were just about back to where we started.

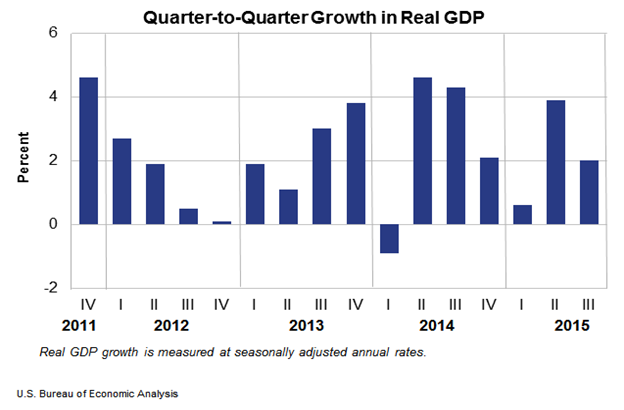

The US economy on the other hand had a fairly good year averaging over roughly 1.75-2.00% annual GDP growth based on preliminary Q4 results. Even though the average growth of the economy over the past 120 years is closer to 3.4%, in light on the ongoing fiscal and monetary challenges across the globe, 2.00% was respectable. Results over the past few years continued to be lumpy as shown below.

2015 was a year of both the good and the not so good. The good includes the Federal Reserve Open Market Committee finally raising the benchmark fed funds rate by ¼ of a point in December after hinting at such a move since mid-2014. This sets the Fed on a path to return to more normalized interest rates, a long-term positive. The not so good includes the Fed Balance Sheet bloated at $4.5 trillion, meaning we will continue to have further uncertainty while this amount is reduced to an equilibrium level.

More good news was the decline in oil prices to levels not seen in over ten years. In 2015, West Texas Intermediate Crude, the US benchmark, declined by 30% and now trades just under $30/barrel. Retail unleaded gasoline is generally below $2.00/gallon across the US. This is a direct and positive cash infusion into nearly every household in America allowing for greater savings or increased spending, both of which are good for the economy. Unfortunately many high-paying energy industry jobs have been lost and more than one energy company has declared bankruptcy or is seeking court protection to reorganize, which will also impact the US banking system holding tens of billions of dollar in loans backed by these companies. So this economic tailwind involves its share of underlying headwinds.

The US dollar proved to be quite strong throughout the year putting increased pressure on exports and correspondingly on corporate profits. Our 2014 Year-End client letter discussed this in greater detail. The dollar appears to have stabilized at current levels, but increasing interest rates in the US in the absence of stronger growth overseas will push the dollar higher versus other currencies. This push will continue to challenge export oriented US companies, but simultaneously keep inflationary pressures in check.

The US headline unemployment rate was 5.0% when last reported. Keep in mind during the darkest moments of the great recession this rate topped 10%. Regrettably as employment improved the ratio of workers becoming disaffected increased such that the Labor Force Participation ratio declined to record lows at 62.5%, meaning a substantial number of potential workers have quit looking for employment. Average hourly wage rates likewise have remained nearly flat, increasing just 2.5% year over year.

The Personal Income & Outlays report recorded high income for Americans of $15.6 trillion accompanied by a personal savings rate of 5.5% – a solid number. Yet the Consumer Credit Report indicates we have record high levels of consumer debt, topping $3.5 trillion, and most disturbing is that Student Loan debt is over $1.3 trillion, whereas at year-end 2008 it was just $730 billion, a near 50% jump.

For some the economy has provided higher income and wealth creation, but many Americans are not participating or benefiting. The US is experiencing high and increasing levels of income distortion. Our national legislators need to develop long-term comprehensive policies in order to create a playing field upon which many can compete and partake in the American Dream.

Although our firm has been cautious over the past few years for many of the reason noted above, at present we are actually very optimistic. We see encouraging signs of improvement ahead. We think Congress has shown signs of improved function and an appreciation that the public is dissatisfied on many fronts. We believe positive change is afoot for our legislative policy makers as well as our monetary policy makers. We believe US industry has been very rational throughout the recession, making careful capital allocation decisions, protecting market-share and profit margin.

Global GDP growth is forecast to be 3.00% in 2016. We think it can be higher as the outlook in the US improves. The US has an $18 trillion GDP. The number two global economy is China with a GDP of about $6 trillion. A robust US economy has the ability to skew global growth either up or down.

Stock market participants have taken a decidedly more negative view over the past year. This has resulted in many companies now having share prices trading at sharply undervalued prices.

Investment Strategy:

Our firm concentrates on investing in the shares of companies when we can buy a dollar of business for 50 cents. The value of a company’s stock fluctuates far more than the value of the company itself. In past letters we have provided numerous examples of market pricing inefficiencies. Any experienced Wall Street investor can attest to the often nonsensical volatility of share prices on a given day.

We believe outsized return-on-investment can be achieved as a consequence of inherent inefficiencies in the public marketplace. The biggest unknown in our strategy is the timing of the realization of our return. We do know from experience that share prices tend to move dramatically over short periods so the ultimate recognition of return may occur very rapidly after many years of patient monitoring.

This point is reinforced in Security Analysis, the definitive text on stock and bond valuation (page 476):

Obviously the stock market is quite irrational in thus varying its valuation of a company proportionately with the temporary changes in its reported profits. A private business might easily earn twice as much in a boom year as in poor times, but its owner would never think of correspondingly marking up or down the value of his capital investment.

This is one of the most important lines of cleavage between Wall Street practice and the canons of ordinary business. Because the speculative public is clearly wrong in its attitude on this point, it would seem that its errors should afford profitable opportunities to the more logically minded to buy common stocks at the low prices occasioned by temporarily reduced earnings and to sell them at inflated levels created by abnormal prosperity.

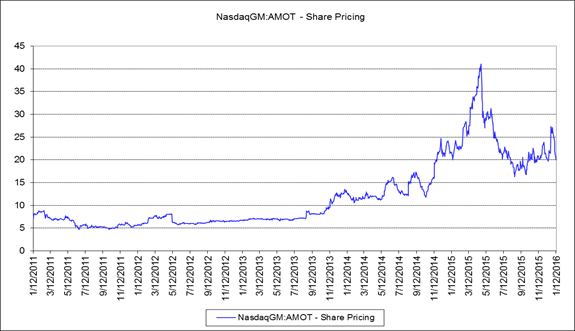

We provided an example of this in a prior letter with Allied Motion Technology (AMOT). This has been a classic example of short-term price variability (see above).

We made an initial investment in the shares in mid-2012 at $6.00. We monitored the company and communicated with management over the next few years. The share price moved modestly during this period. Then in mid-2015, very suddenly and without significant new information to impact valuation, the shares moved sharply higher. We used this circumstance to sell shares once they exceeded our price target. Again, without any significant news, the shares dropped to a level consistent with the pre-move pricing.

This clearly demonstrates how shares of publicly traded companies can be bought at discounts and sold at premiums. Patient investors stand to earn attractive return-on-invested capital over time if they can identify when shares are undervalued and overvalued and execute buy and sell trades at those times.

We spend the majority of our working day analyzing the value of companies. As discussed in the past, we study company financial statements and are thus able to base our appraised value on those numbers. We find share prices often move without any reason connected to the business, but more, we suspect, by the emotional disposition of the most reactive investors.

Investor psychology certainly influences share pricing. This must be acknowledged. The question is does the emotion represent rational thought and behavior? We think it often does not.

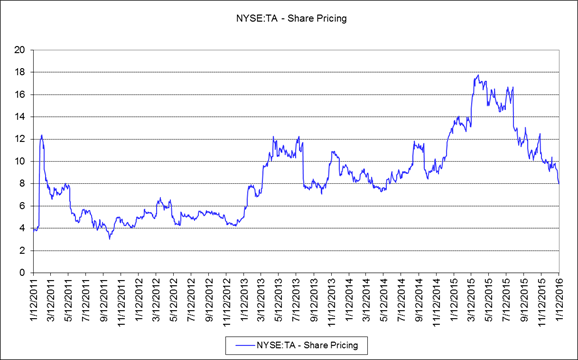

The above share price chart is that of TravelCenters of America (TA). Note the price variability over the short-term in which the share price rises and falls by 50% or more. The financial condition of the company had changed only modestly during those time period, yet the share price swings were radical, not in proportion to the underlying economic change in the condition of the company.

Our strategy allows us to appraise a company and arrive at a valuation on a per share basis. With this we can easily match the current share price quote with our apprised share value and invest when we feel a substantial discount exists. Our goal is to invest when we believe shares trade at a 50% discount.

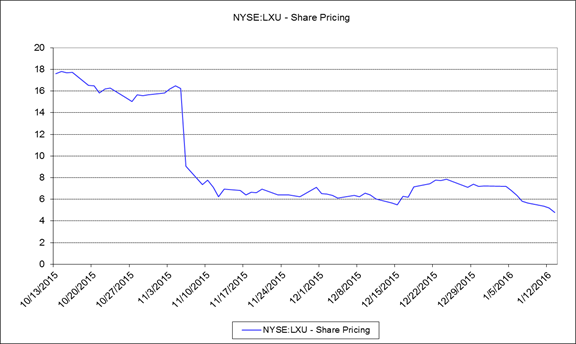

The share price of LSB Industries (LXU) declined rapidly as news developed of plant construction overruns that were transitory in nature. The share price declined well beyond a level that reflected the impact of the cost overrun. The graph below shows the recent sharp price decline.

As indicated earlier, market participants can be irrational. There are no rules surrounding market participant reasonableness, thus a company trading at a 50% discount can trade lower, say to a 60%, 70% or even greater discount as illustrated with LSB Industries.

We like to think the day we announce our buy decision all other market participants will recognize our wisdom and “Buy, Buy, Buy,” to quote Jim Cramer, but that usually doesn’t happen. However, we are protected by virtue of our conviction in our research and analysis as well as our long-term investment horizon. We have the advantage of patience.

We measure investment outcomes over three to five year periods. We think any shorter perspective encourages speculative trading behavior. We think companies produce results over years and those results are ultimately reflected in the value of a company’s equity and share price.

We acknowledge there are no good comparative benchmark indices against which to measure ourselves because we manage money for clients the same way we mange for ourselves, being fundamentally risk averse and willing to commit capital only when we find suitable investments. Unlike most indices, we are indifferent to the size of a company, its economic sector, its geographic locations, and other fashionable metrics. We simply concentrate on the current gap between our appraised value and the last quoted share price, and are willing to hold cash while we wait for bargains to appear.

In any given period, whether a calendar quarter or a year, we will only rarely produce results that match the market index. We accept that when we choose to manage money differently than the way an index is managed we will necessarily produce different results. Over time we expect to produce significantly different and superior results.

We own a number of companies that meet the criteria of being sharply discounted and have become more so since we added them to our portfolio. Some of those are listed below:

| Company( Ticker) | Share Price | Appraised Value | Discount |

|---|---|---|---|

| StealthGas (GASS) | $3.00 | $8.00 | 60% |

| TravelCenters (TA) | $8.00 | $24.00 | 65% |

| LSB Industries (LXU | $5.00 | $33.00 | 70% |

These companies have all been thoroughly researched and analyzed and realistic price targets established. Our research team regularly communicates with senior management and reviews all financial releases. We believe each of these companies will ultimately reach our appraised value. We continue to update our analysis as additional information becomes available.

Firm Update:

As indicated in our 3rd quarter letter, the firm went through a reorganization in August of 2015. Our ownership remains the same but other exciting changes have occurred. We created a holding company structure and named the parent company Global Value Investment Corp (GVIC). We have three divisions within GVIC, including Milwaukee Private Wealth Management – our original advisory business serving individuals and families; Milwaukee Institutional Asset Management – offering services to other investment professionals; Global Value Research Company – encompassing our investment research teams in Milwaukee and Hyderabad, India.

This name change reflects the growth in the firm’s business strategy and clientele over time.

Concluding Thoughts:

Since 2007 we have been fortunate to be able to manage assets for a broad range of clients. Please let us know if you have experienced any meaningful changes with your investment objectives so we can update our files.

Over the years we have experienced some wonderfully successful investment outcomes and others less so, but have always enjoyed coming to the office and exercising high levels of effort and creativity to maximize our return-on-investment. We expect to continue to do so for many years to come and thank you for your ongoing confidence in us and the firm.

Very best wishes,

Your Investment Research and Advisory Team

Global Value Investment Corp.