Outlook:

2018 got off to a rocky start with increased market volatility and heightened economic and political uncertainty.

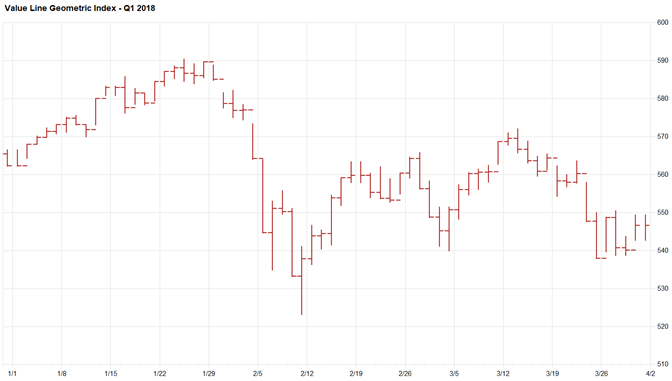

Broadly measured, the stock market closed out the first quarter of the year declining 2.8%. During the quarter, we witnessed dramatic price swings. Stocks declined by over 11% from late January through mid-February. Between March 21st and 23rd, the market dropped nearly 4%, shaking investor confidence. We’ve not see this type of price volatility for a few years.

For example, General Electric, once considered among the bluest of blue-chip stocks, dropped from a high of $19.40 to a low of $12.40 during the quarter, a decline of 36%. Looking back one year, GE fell more than 53% from a high of over $30.00. Virtually no company has been exempt from recent price fluctuations.

Looking for root causes of this volatility, we observe the US economy has experienced comfortable growth, expanding by 2.9% in Q4 2017 – clearly not a reason for concern. Forecasts for Q1 2018 GDP remain in the 2.5% range. Stocks advanced firmly going into Q1, after a significant tax reform bill was signed into law, cutting corporate tax rates sharply, from 35% to 21%. Unfortunately, Individual tax payers didn’t fare as well, with many long-standing deductions being phased out at much lower levels, if not eliminated altogether. The tax reform excitement appeared to cause prices to head higher into the new year with continued momentum until late January, when the market correction began.

Shifting to monetary policy, the reality of higher interest rates was reinforced with the change of leadership at the Federal Reserve Bank as Janet Yellen passed the gavel to Jerome Powell on January 31st. Powell’s appointment coincides with the beginning of the recent spate of price fluctuations. It would seem that the markets expected a more dovish Fed Chair, which apparently is not going to be the case. Powell quickly put the markets on notice that interest rate hikes were very much on the table. At its March meeting, the Fed’s Open Market Committee hiked again, raising overnight rates to a range 1.50% – 1.75%, a considerable increase from the 0% – 0.25% range last seen in December 2015. Higher interest rates will unquestionably put downward pressure on stock and currency markets around the world.

Adding to the drama with interest rates was the initial escalation of import tariffs floated by the Trump administration. A US-imposed set of global steel and aluminum tariffs, as well as tariffs specifically targeting the Chinese, dominated the news for several weeks.

Overlaying this was the Olympics, featuring a possible thawing of tensions between North and South Korea, while ongoing posturing between the US and North Korea over its nuclear weapons program persisted. It is understandable why market volatility is heightened.

With all this noted, we continue to think solid underlying economic fundamentals will allow continued growth in earnings. We remain cautious, however, with respect to stock and market valuations. We sense many stocks have become substantially overvalued given the prospects of moderate economic growth. Rising interest rates and growing signs of inflation will necessarily cause valuations to contract. Those stocks most extended will likely suffer the largest declines in a process that brings valuations back in line with long-term, normalized trends.

Perspective – Prices Fluctuate More Than Value:

From the April 1st, 2018 issue of Barron’s weekly newspaper:

Many investors are now learning that, because of the dominance of the tech sector in indexes weighted by market cap, they aren’t as well-diversified as they had thought. Technology stocks accounted for more than 25% of the S&P 500 at the end of February, and just five stocks — Apple, Microsoft, Amazon, Alphabet, and Facebook – accounted for 14.4%, far exceeding the weighting of other sectors like industrials.

These tech issues are among the most overvalued stocks in the market today.

At Global Value Investment Corp., we invest in companies that we believe are underappreciated and mispriced by other market participants, avoiding the more popular and frequently-overvalued issues. We concentrate our analysis on business fundamentals, studying financial statements, industry trends and management’s strategic plans. We focus on just a handful of companies in which we think we have developed an information advantage by understanding the business and the reasons for the mispricing. We invest when we believe a stock’s price is substantially undervalued in relation to its business value. When we invest, we act as though we’re buying the entire business and interact with management accordingly, holding management accountable to shareholders.

As a result, we spend little time thinking about stock indexes or how we perform in comparison. Our focus is on investing in companies that are mispriced by market participants. For example, when we can invest and own a business at 40% – 50% of its asset value, we believe that over time, we will have a favorable investment outcome. We enjoy a long-term investment horizon, which benefits us and our clients when it comes to achieving an acceptable return on capital.

The following are just a few of the business we hold in client accounts:

Stealth Gas (GASS) trades for ≈$4.00 and has a current book value of ≈$14.40

Seaspan (SSW) trades for ≈$6.75 and has a current book value of ≈$13.30

Gulf Island Fabrication (GIFI) trades for ≈$7.25 and has a current book value of ≈$14.70

Bristow Group (BRS) trades for ≈$13.00 and has a current book value of ≈$35.25

Each of these companies has an experienced management team with whom we regularly communicate. Several of these businesses hold dominant market share in concentrated or consolidating industries. We believe that over time, as fundamentals improve, other market participants will come to recognize the mispricing and bid up share prices to close the discount gap, at which point we will consider exiting the investment in search of other mispriced situations.

As is apparent in the case of GE, large, popular and broadly-owned stocks are subject to sharp share price declines. If an investor overpays when purchasing a stock, they may spend years, if not decades, recouping their investment. We attempt to invest only after a stock has declined to a price that represents a sharp discount, which has made investing over the past few years all the more challenging given the infrequent appearance of such issues. We remain vigilant – and somewhat more excited – as we witness the heightened level of price volatility, seeking opportunity to commit capital to undervalued businesses.

From Our Library:

One of our favorite investment reads, originally published in 1949, is The Intelligent Investor by Benjamin Graham. The following excerpts hit the nail on the head when it comes to successful investing:

To invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework. (pg. ix)

A great company is not a great investment if you pay too much for the stock. (pg. 181)

The intelligent investor gets interested in big growth stocks not when they are at their most popular – but when something goes wrong. (pg. 183)

Price fluctuations have only one significant meaning for the true investor. They provide him with an opportunity to buy wisely when prices fall sharply and to sell wisely when they advance a great deal. (pg. 205)

The investor with a portfolio of sound stocks should expect their prices to fluctuate and should neither be concerned by sizable declines nor become excited by sizable advances. He should always remember that market quotations are there for his convenience, either to be taken advantage of or to be ignored. (pg. 206)

The intelligent investor should recognize that market panics can create great prices for good companies and good prices for great companies. (pg. 483)

We recommend this book to all – both new and experienced investors.

Firm Updates:

Global Value Investment Corp., the parent of Milwaukee Private Wealth Management, now produces investment research through its Global Value Research Company division. The firm recently began distributing its research through three independent, global market channels. The very same reports are available to Milwaukee Private Wealth Management clients. If you would like to read more about the companies in which you are invested, please let us know and we will be happy to send periodic reports.

One of our young associates, Sam Schaefer, has decided to pursue other interests. We wish him the best of luck and thank him for his nearly four years of dedicated service to the firm.

Our India research subsidiary is strong and growing. We are celebrating one year with the team officially in place – they have provided extraordinary input and perspective from 9,000 miles away.

Concluding Thoughts:

We are always mindful that we are investing other people’s money and as such have a great responsibility to apply rigor in every decision. The firm has a policy that each of its associates will invest in the very same issues we recommend for addition to client portfolios, a policy we think wise and one we would expect if our roles were reversed.

As always, we thank you for the ongoing confidence, trust and the kind words we often hear. Your support means a great deal to us, particularly when stress levels rise due to unanticipated events or increased price volatility. If you’ve had a change in, or would like to update, your investment objectives or portfolio restrictions, please let us know so we can make appropriate adjustments. We recently filed our updated form ADV with the SEC. Please let us know if you would like to receive a copy.

We continue to commit ourselves to achieving investment excellence over time.

Your Investment Research and Advisory Team

Global Value Investment Corp.